A satisfying transaction

Editor's note: Tony Smith is the global head of financial services research for Ipsos. He is based in London.

Anyone who’s used a dating app will tell you that virtual dating isn’t the same thing as meeting someone in person. Sure, you can build an emotional bond of some sort but if that online connection doesn’t translate into the real world, the relationship is over before it begins. Anyone who’s used a dating app will also tell you that apps have forever altered the experience of dating.

In the same way, the world of banking and financial services has changed dramatically in recent years. There was a time, not long ago, when interactions with a bank were largely face-to-face. The first disruption was call centers that gave us a convenient alternative, allowing us to do many things outside of branch hours. We could verify account balances, transfer money, pay bills or even discuss available home-financing options while still interacting with humans. We didn’t even need to venture outside of the house. The next disruptions came in the form of online banking, price-comparison sites, mobile apps to manage our accounts, digital wallets, robo-advice and live chat – all services that offer convenience for consumers.

And as consumers have adopted technology in their everyday lives for everything they do, non-traditional financial services players (fintechs and insurtechs) have developed and now play a key role in meeting consumer financial needs particularly in payments and in the insurance and investment arena. Legislation will have an impact, too. The PSD2 directive in the EU looks set to be the next Uber moment in the financial landscape. While this impacts EU nations right now, it is being closely watched by banks and other financial providers around the globe. It will expand opportunities for banks and fintechs alike and will spawn ever more new technology-driven business models with great potential customer appeal.

PSD2 will mean that banks must grant third-party providers access to a customer’s online account/payment services data with the customer’s permission. The bank will no longer “own” the customer’s data and companies will be able to use that data to potentially provide better products and services. E-commerce sites such as Amazon could become the payments processor rather than MasterCard, Visa or PayPal.

Set to continue

Digital disruption in financial services looks set to continue and banks should be concerned that increasingly in banking, unlike in dating, the relationship doesn’t necessarily have to transfer to in-person!

It is not all doom and gloom for banks though. Research from Bain in 2016 showed that growth in mobile banking is leveling off in many countries and actually declined in 2016 in China. At the same time the decline in the use of call centers and bank branches is slowing. There’s still a need for branches, despite the seemingly neverending march to closure in some parts of the world. Indeed, Bain’s findings showed that around 40 percent of people who had experienced a branch closure took their business elsewhere. The implications of this are obvious – not everyone wants digital for everything or, if they do, perhaps it doesn’t fulfill their needs and expectations sufficiently yet. Banks still need to develop the omnichannel approach for customers and understand the requirements and perceived limitations of the various channels for different needs.

Whatever the case, the pace of digital change will continue and relationships will become more and more remote. Human interaction, long seen as the opportunity to create an emotional connection with the customer, will continue to decline. So too will the chance to provide exemplary customer service.

Build an emotional connection

Ipsos research shows that it is important to understand how to build or maintain this emotional connection. Why? Because you only reap the benefits when you do!

Our study among 800 consumers in the U.K., U.S., France and Germany looked at banking, auto and mobile network providers. The research helps provide a framework for understanding the importance of building an emotional connection (meeting emotional needs) over and above meeting a customer’s functional needs.

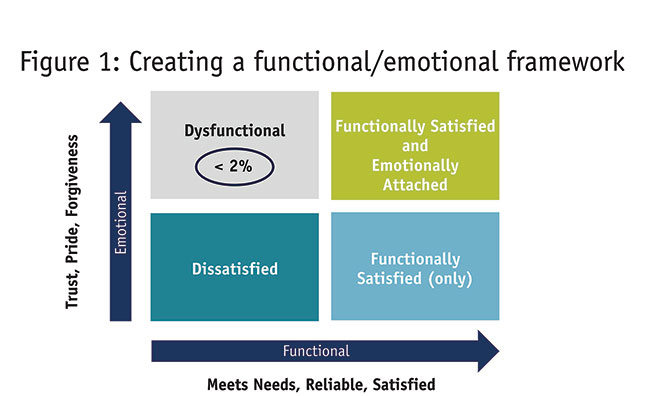

It’s worth understanding the differences between meeting emotional needs and meeting functional needs and how we distinguish between the two in our research (Figure 1). Functional needs are those aspects of the experience that are included in many customer experience evaluations: ratings on aspects such as speed, accuracy, competence and content. These are tangible aspects of the service or experience. Emotional aspects reflect a connection with the supplier, including rating a company on dimensions such as “how close do you feel toward [brand],” to what extent you’d be “willing to forgive [brand] if it made a mistake,” “feeling a sense of pride for being a customer of [brand],” “I would trust [brand] to do the right thing.” Each of these implies a sense of emotional connection with the brand.

The first point to make is that very few (less than 2 percent) people rated their brands highly in meeting emotional needs while also rating them low on fulfilling the functional aspects. This makes intuitive sense – if a brand doesn’t do the basics consistently and reliably and if a customer rates them poorly in terms of overall satisfaction, it is unlikely that the customer will have an emotional connection with the brand.

What this then gives us is a continuum. At one end are customers for whom neither functional nor emotional needs are met. Further along are those who are functionally satisfied but not emotionally connected to the brand. Finally, there are those customers who are both functionally satisfied and feel attached to the brand (Figure 2).

Importantly, for a brand to make an emotional connection, it must meet a customer’s basic needs. Customers will only be proud to use your brand and trust you (to do the right thing for them) if you get the basics right for them consistently. In today’s world of constant and sometimes-viral feedback, it’s also important to know that they will also be more likely to forgive you if something goes wrong.

It could be argued that, if the key aspect of a relationship is getting things consistently right, that should be the business’s focus. Let’s look at the checking account customer of a bank. If you process their payments on time, don’t overcharge, don’t make mistakes and make it easy for them to transact, then that customer will continue to be a customer. There is a strong likelihood that they will remain a customer in the future if they are functionally fulfilled, unless something changes or entices them away. After all, few people actually switch banks in any one year.

But – and this is a big but – as the schematic in Figure 3 shows, it is only when you establish an emotional connection with the customer that you get the step-change business outcomes that many organizations strive to achieve.

If a customer is both functionally satisfied and emotionally connected to the brand:

They are more than 25 percent more likely to stay with the brand in the future than if they were simply functionally satisfied.

They are almost twice as likely to recommend your brand.

Their likelihood to consider your brand for their next product/service when the time comes increases by nearly 50 percent more than if they were simply functionally satisfied.

But how do we build emotional connections in largely functional relationships when these functional relationships are becoming more remote due to the adoption of digital channels?

Undermine or build

What kinds of things have you done that might make a customer dissatisfied? Or delighted? It tends to be these memorably bad or good moments that either undermine functional satisfaction or build emotional connection – Web sites being down, confusing offerings, long wait times for customer service, lack of response, inexplicable payment rejection, etc. Conversely, emotional attachment can be nurtured through responsive and proactive customer service; exceptional handling of issues; going out of your way to help; well-designed user interfaces and user experiences and products that do what they say they will and deliver on promises of speed and convenience. Identifying which “memorably good” moments of service or “memorably bad” moments have the greatest impact on your customers is critical to understanding what action you need to take.

Critical incidents make or break loyalty. In human relationships, maximizing these events is increasingly the difference between a happy experience for one customer that might be shared among family and friends and a viral video or Yelp rant that might be spread among thousands of potential customers. Having systems in place to address and respond to customer issues can help staff foster the loyalty-forging moments they’ll remember. Technology can be an asset to monitor and manage continuous customer feedback and resolve critical incidents.

In virtual relationships, many of these issues come up as well. But in these relationships the customer is left to sort it out himself. Understanding how to optimize the omnichannel experience for the virtual customer, via the use of chatbots and other digital help for example, is critical. Yet that warm customer voice or handshake may be necessary to make the experience work. That’s especially true for the customer who has spent several minutes doing a seemingly simple task only to hit a brick wall!

In short, make it easy. Functional, fast apps with great interfaces will help forge that connection if they allow customers to accomplish what they want with minimal disruptions. Uber’s most-basic “disruption” was nothing more complicated than a straightforward app. Allowing customers to hail a ride when they wanted it rather than standing out in the cold and rain with their arm raised hoping an unoccupied cab drove by was a game changer in an otherwise tech-free industry. The taxi industry could have maintained its established dominance if it had moved at the right time to create a product that would appeal to a new generation of customers. In the absence of leadership from the established brands, a start-up was able to move in and create new space. This is happening and could continue to happen to banking and financial services, too.

Well-positioned

That said, the existing players are well-positioned to head that off if they act. They already have longstanding and loyal relationships with customers as well as trust. They have a trove of customer data which can be used to make suggestions and train AI apps to help the customer. They are already doing so through simple things such as proactive alerts about balances or rates and by filling in fields with existing data rather than making customers fill them in again and again. As the technical and legal climate changes, as we are seeing with PSD2 in the EU, competition will increase in the digital financial world. Traditional players need to take every opportunity to work with the customer in his technological world to make the virtual vs. human interface as personable as desired so that both parties win. It is more important than ever to think through ways to maintain and manage the functional and emotional connection of the virtual world with the real-world consumer.

References

Bain and Company: Customer Loyalty in Retail Banking: Global Edition 2016.