Editor’s note: Philippe Rondeau is project manager, client operations, at research firm Kantar, Paris. This is an edited version of a post that originally appeared under the title, “Brand buying loyalty: What makes consumers go back again and again?”

In a time when choice is rife for consumers and disruption regularly produces new opportunities, understanding the factors that help or hinder your brand to be chosen by customers is vital. I was recently involved in a Kantar study that explored the reasons consumers stay loyal in their reported buying behaviors, as well as the motivations to switch brands. We interviewed 3,657 people from the Kantar Profiles Network across 12 countries (U.S., Brazil, U.K., France, Germany, Spain, the Netherlands, India, Singapore, Indonesia, mainland China and Korea) covering 11 categories of products and services.

Loyalty is largely skewed toward services

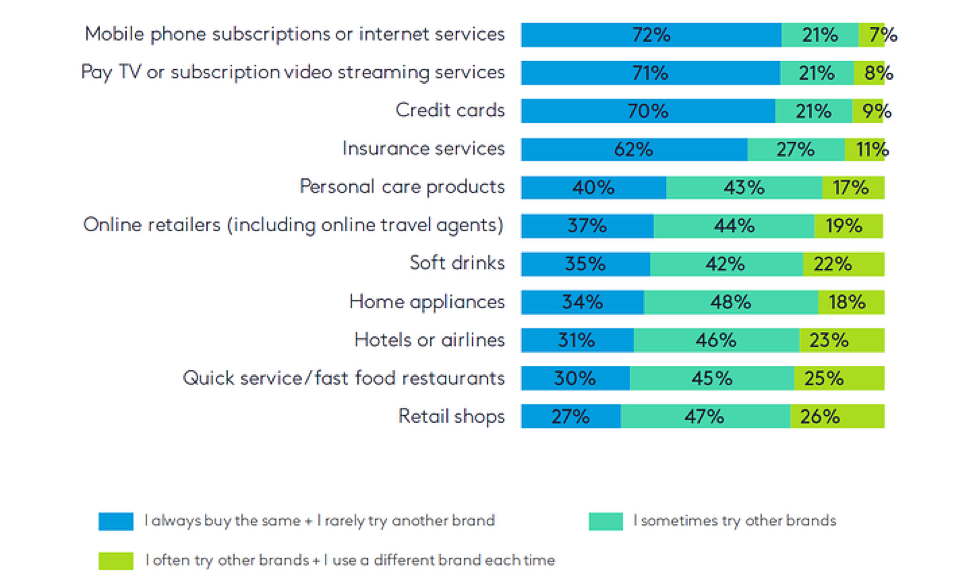

The level of loyalty reported by respondents varied significantly across categories, as displayed in the chart below. The top four categories, however, were all-serviced based, with mobile phone subscriptions/internet services, pay TV or subscription video streaming services, credit cards and insurance services ranking highest for global loyalty. You can see a notable drop at personal care products (40%), ranking fifth, as loyalty continues to decline in consumer product categories.

Price and quality matter most

Price and quality matter most

The circumstances around choosing different categories of products and services varied greatly. If we look at the reason’s consumers choose to remain with the same brand, however, cost and knowledge of quality were reported to be the most influential for 90% of consumers. Habitual factors were the least impactful, with repeat purchases and “never having tried anywhere else” reported by just 35% of respondents.

Price sensitivity – key factor for loyalty

Eighty-seven percent of consumers interviewed reported to shop around for the best prices and deals. This statement is reported for all the categories of product or services.

Impact of new releases

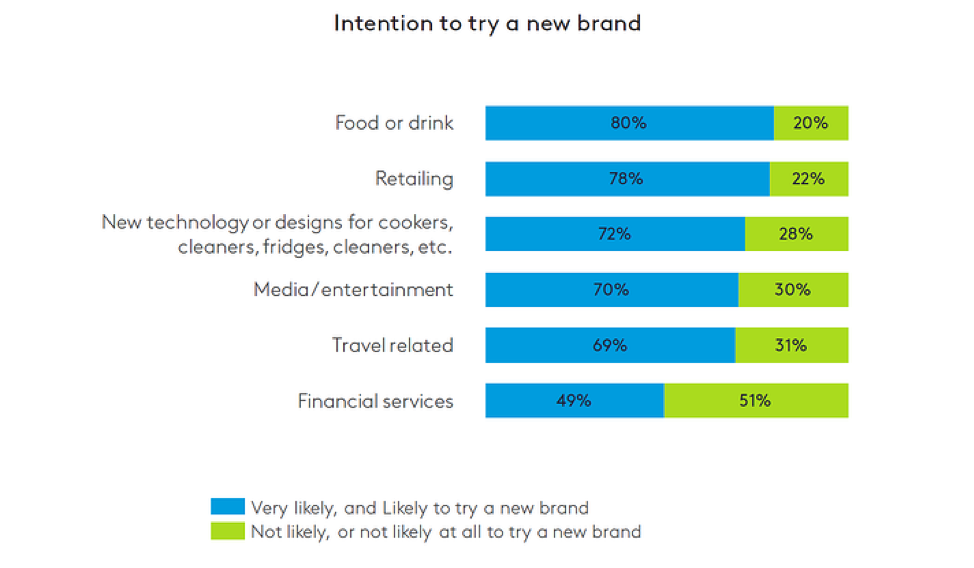

How likely are consumers going to be willing to test out a new brand in the marketplace? Eight out of 10 respondents stated they are “in with the new” when it comes to trying food and drink brands. Retail (78%) had a similarly high propensity, whereas financial services had the lowest intention to try a new brand (49%). At an overall level, defection appeared to be significantly higher in Asia and Americas regions than in Europe.