Are they really that different?

Editor's note: Lesley Brooks is senior vice president at Radius Global Market Research, New York.

Much has been made of the generation gap between Millennials (18-32-year-olds) and Boomers (49-67-year-olds). Conventional wisdom and countless lifestyle surveys verify that the two groups indeed have differences in attitudes and outlooks on life. This has fueled a movement of marketers looking closely at how to harness the buying power of each group and to adjust plans accordingly.

But before launching segmented strategies, perhaps marketers should take a closer look at these consumer sets – specifically how they shop – to see how wide the generation gap actually is. Are spending behaviors different enough between Millennials and Boomers to represent an opportunity to increase profits via a segmented approach? Are differences today likely to be there tomorrow? Are the purchase requirements and influencers distinct enough in every category to merit separate marketing messaging and media plans?

A recent study of Millennial and Boomer buying behaviors including channel usage and key influencers conducted by our firm explored how Millennials and Boomers compare when it comes to spending on goods and services across a number of categories. The study set out to provide a deeper assessment of buying behaviors, requirements and priorities. The online study surveyed a nationally representative sample of U.S. consumers – all members of the Millennial or Baby Boomer generations.

Findings indicate there are indeed notable differences between Millennial and Boomer shoppers as they navigate purchases – in general and across key product and service categories. But there are also important similarities that should also be considered as marketers plan.

Relatively optimistic

When it comes to the U.S. economy, a majority of both Boomers and Millennials are relatively optimistic about the outlook. But Millennial shoppers are more optimistic, with 71 percent indicating confidence in the future state of the country’s financial affairs. Boomers are less likely to be optimistic about the nation’s financial outlook. It’s also interesting to note that while Boomer men are optimistic (66 percent), fewer Boomer women (53 percent) are confident that economic conditions will improve.

When asked about spending patterns (compared to usual) during the recession, both groups were generally conservative. As further evidence of their optimistic edge, Millennials were more apt to maintain or increase their spending (55 percent) during tough economic times. Boomers, on the other hand, tended to pull back on spending, with 60 percent making cuts. Twice as many Millennials boosted spending compared to Boomers.

Millennials and Boomers have a similar set of concerns that drive purchases. Both groups tend to focus primarily on quality, price and value, depending on the category. Millennials as a group are relatively more price-conscious than Boomers.

Taking a look at anticipated spending habits, when Millennials and Boomers were asked to identify the categories in which they are likely to increase spending in the year ahead, the category sets are essentially the same: apparel, packaged foods, travel and financial products/insurance.

Where the two groups differ is in their priorities. Millennials place travel and apparel as their top two priorities for increased spending in 2014. Boomers are more focused on “necessities,” ranking packaged foods and insurance products higher. Interestingly, while both groups spent more on electronics (including smartphones, tablets and home entertainment systems) in the past year, neither anticipates increasing spending in this category during 2014.

Millennials and Boomers also share the same habits when it comes to where they shop. Retail is by-and-large the prominent channel for buying most everyday packaged goods, apparel and electronics. Online is the preferred channel when it comes to purchasing travel for Millennials (70 percent) and for Boomers (90 percent). Of all respondents, female Boomers are least likely to order products online. Also, female Millennials are not shopping online for PCs, insurance or banking accounts at the same rate as their counterparts.

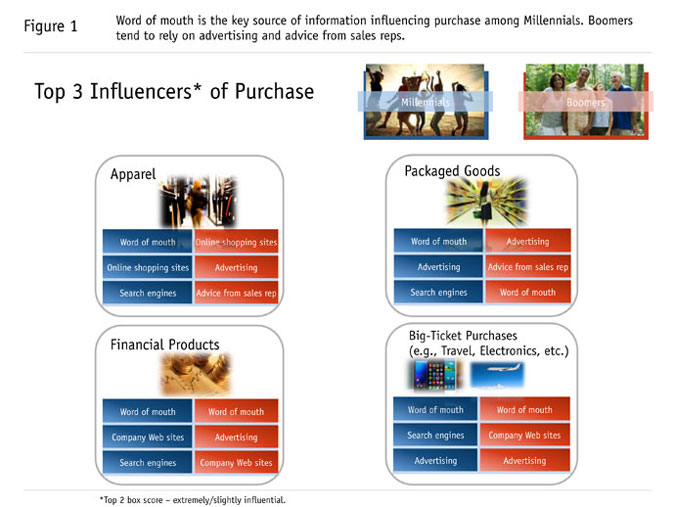

Millennials and Boomers differ when it comes to what they say is the most influential source of information during the purchase process (Figure 1). Word-of-mouth is the most important source influencing Millennials across all key categories. Search engines are also a factor in all categories but they hold slightly less influence than word-of-mouth.

Boomers tend to be influenced by traditional advertising and advice from sales reps. An exception to this is travel purchases, where Boomers are swayed primarily by word-of-mouth sources and, incidentally, do a very high percentage of purchasing online.

Shopping trends indicate that while marketers should expect to see both Millennials and Boomers using the same purchase channels, they should be prepared to leverage different influencers and different product features, depending on the group they are looking to engage.

Active product researchers

Boomers and Millennials are active product researchers. PCs are the primary means for accessing product information, with 90 percent Millennials and nearly that many Boomers (86 percent) using a computer to conduct research. As expected, product research via smartphone is higher among Millennials, with 60 percent saying that they’ve used the device for this purpose. And a full 20 percent of Millennials indicate that smartphones are their primary device for conducting product research.

By contrast, only 14 percent of Boomers say they use a smartphone to access product information. And there is still a role for more traditional media, as 38 percent of Boomers will consult newspapers and magazines for information, twice the rate of Millennials.

But, as it turns out, new media and technology are not just for the younger set. While still below the usage rates of Millennials, Boomers are embracing new communication platforms. More than 70 percent of Boomers say they text. Virtually all Millennials do. Both are engaging via social media at healthy rates. For example, female Boomers and Millennials use Facebook at a nearly identical rate (90 percent). And streaming movies and television programming is a reality for both Millennials (77 percent) and Boomers (40 percent).

Boomers’ usage rates of the newer media still lag behind Millennials. A third of Boomers use Twitter but two-thirds of Millennials do. Half of Millennials, but only 10 percent of Boomers, use Instagram.

While Millennials are using newer technology at a higher rate, marketers should realize that the pattern of adopting new technology among Boomers is similar to that of their counterparts. Millennial use appears to be a good predictor, as Boomers are gravitating toward the same devices and platforms. They are just one or two steps behind.

Key findings in categories

The degree to which the similarities among and differences between Millennial and Boomer shoppers show up in market varies by category (Figure 2). Here are some key findings in categories where both groups are actively spending.

Apparel

While both Millennials (81 percent) and Boomers (76 percent) bought apparel in the past six months, a larger number of Millennials spent more this year than in the previous year. More Boomers scaled back their apparel purchases in the same period.

Both Millennials and Boomers say that price and quality are the top two factors impacting purchases of apparel. Millennials tend to pay attention to price first. Boomers look at quality first. Most Millennials and Boomers shop for apparel in a physical retail store. Millennials are more likely to do so online.

Online sources like search results, retail sites and social media, coupled with word-of-mouth, are influencing Millennials’ apparel purchases. Boomers were significantly less influenced by these sources.

Dining

In dining, both Millennials and Boomers frequent restaurants at nearly the same rate: six-to-seven times each month on average. Specifically, in the previous three months, Millennials visited restaurants an average of 21.7 times and Boomers made 18.8 visits in the same period of time. The number of visits, however declines markedly with age among Boomers. Boomers under 55 years of age visited an average of 22.2 (on par with Millennials) but average visits from Boomers over 60 dropped to 15.6.

One-third of Millennials are spending more in restaurants compared to a year ago. Less than one-quarter of Boomers are. Next year, fewer Millennials and Boomers anticipate spending more when they dine out.

Quality is the leading factor impacting restaurant selections for both Millennials and Boomers. Price is next for everyone except Millennial females, who look at type of food before price when making their decision.

Travel

In the travel category, the purchase behavior of Millennials and Boomers is strikingly similar. They are traveling at the same rate, with roughly one-quarter making a purchase in the past six months. Both are also similar in what factors impact purchase: price, value and quality, in that order. Millennials and Boomers also anticipate the same rates of change in spending, with roughly 40 percent indicating they’ll spend more next year and 13 percent saying they will spend less. Finally, word-of-mouth is the top source of influence when it comes to travel.

Surprisingly, more Boomers (90 percent) made their travel purchases online. And the number of Millennials purchasing travel at a retail stores was three times the number of Boomers.

Packaged foods

Purchases of packaged foods among Millennials and Boomers occurred overwhelmingly at a retail store. Only 10 percent of Millennials and 4 percent of Boomers bought items online. Quality and price are leading factors influencing purchase. While percentages both groups making packaged foods purchases in the past six months were similar, nearly half of Boomers anticipate increasing spending in the category, vs. 39 percent of Millennials. Advertising plays an important role in influencing both, but word-of-mouth is most important to Millennial shoppers.

Look beyond the categories

While it is beneficial to understand the similarities and differences between generational groups, it is also important for marketers to look beyond these overarching categories. For example, study results point to several instances where the gender gap may play as great a role in purchasing behavior as the generation gap.

The gender gap in Millennial consumer purchasing, for example, is most apparent in the financial services category. Millennial females are significantly less likely than Millennial males to have obtained a bank account (26 percent among Millennial males vs. 17 percent among females) or insurance (23 percent to 14 percent) in the past six months. In addition, Millennial males are three times as likely as females to have made a personal financial investment in the past six months (15 percent vs. 5 percent).

In consumer electronics, the purchase levels of Millennial females are also comparatively lower. While Millennials overall are key buyers of electronics/computing devices, Millennial females significantly trail Millennial males in the purchasing of tablets (36 percent vs. 25 percent), smartphones (52 percent vs. 39 percent), PCs (44 percent vs. 34 percent) and TVs/home entertainment systems (54 percent vs. 40 percent).

And, as touched on previously, when selecting restaurants, type of food is a key factor for Millennial females while Millennial males say that value is relatively more important to them.

Nuances such as gender require at least as much attention when it comes to engaging both Boomers and Millennials. If a marketer is focused on Boomers or Millennials as a single group, they may be missing opportunities to optimize engagement, especially when, as the study suggests, the generation gap in terms of purchasing trends may not be as wide as anticipated in any given category.